Call: 888-297-6203

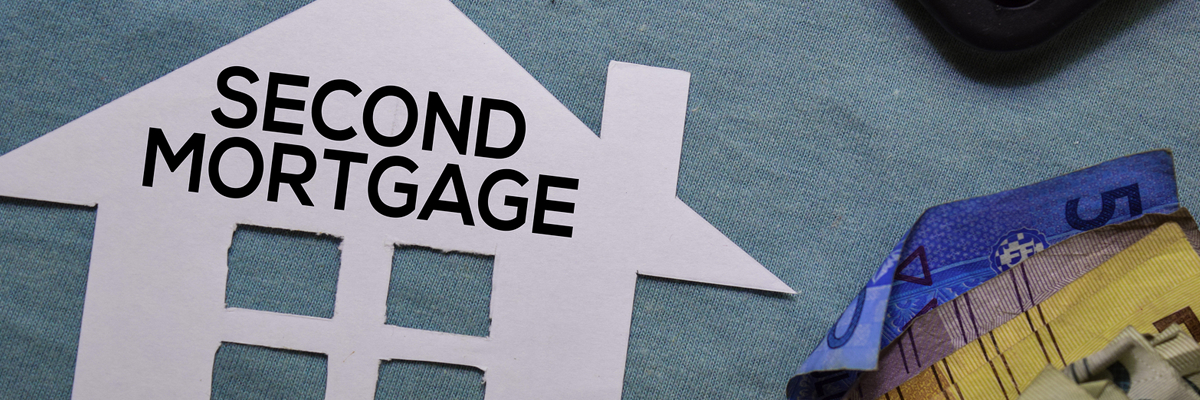

As per the latest ruling by the Eleventh Circuit Court of Appeals, second mortgages can be stripped off in a Chapter 7 bankruptcy case. Lawyers of Los Angeles based bankruptcy law firm Recovery Law Group say, this means that if the amount on 1st mortgage is more than the current market value of the home, the 2nd mortgage is considered as good as unsecured and therefore can be discharged as other unsecured debts are discharged in a chapter 7 bankruptcy. Earlier, this discharging of second mortgage was possible only in case of Chapter 13 bankruptcy cases as 11 USC §506(d) did not apply in case of Chapter 7 cases. The ruling of Supreme Court was modified by the Court of Appeals as despite Supreme Court saying that §506 didn’t apply in Chapter 7 in case of partially secured “cram down” of any bankruptcy filer’s main residential property, this opinion of Supreme Court does not mention any other ways in which it could be applied in a Chapter 7 case.

Sooner or later, a petition will be filed in the Supreme Court regarding whether the statute of discharging second mortgages in case of primary mortgage being higher than current market value of property can be applied in case of Chapter 7 bankruptcy case. However, till this happens, people can protect themselves by getting rid of additional loans. In case you need assistance from best legal minds, you can call 888-297-6023 to discuss your case with experienced bankruptcy lawyers.